Renowned financial analyst Brent Johnson developed the dollar milkshake theory to explain the supremacy of the U.S. dollar and its dominance in the global economy. This article explores the integral role that central banks play in the dollar milkshake theory, examining the reasons behind the dollar’s strength and its impact on the economy.

Overview of the dollar milkshake theory

The dollar milkshake theory asserts that despite uncertainties in the global economy, the U.S. dollar will continue to strengthen relative to other currencies while drawing its liquidity from global markets.

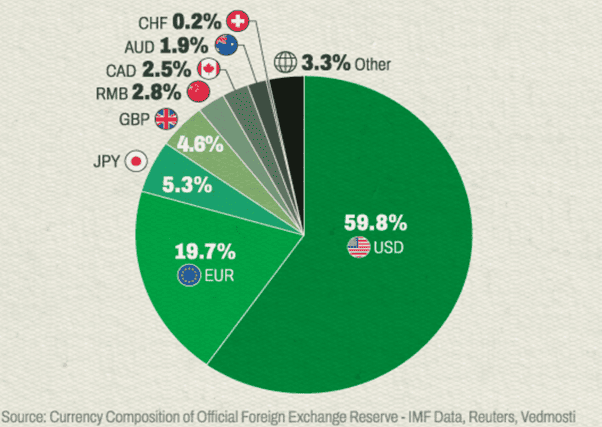

World foreign exchange reserves: CTMfile

Theoretically, the ‘milkshake’ represents the global economy and its liquidity, whereas the ‘dollar’ is the giant straw that keeps sucking its liquidity into the U.S. economy. In addition, the theory proposes that the dollar’s dominance in the global market can be attributed to various factors, including global debt, differences in interest rates, and the relative strength of the U.S. economy compared to other economies globally.

According to the theory, the continued dominance of the U.S. dollar will (and does) destabilize the global system, overburdening other countries with dollar-dominated public debt. Thus, the dollar milkshake theory suggests the U.S. will continue acting as a haven that attracts more capital at the expense of the rest of the global economy. Meanwhile, the reliance on the U.S. dollar across the globe will work to weaken other currencies.

Reasons for the strength of the dollar

The dollar’s dominance stems from its status as the world’s largest and most dominant reserve currency.

This status can be traced back to 1913, when the U.S. economy grew larger than the British economy, and the dollar became more valuable than the Great British Pound (GBP).

This dominance was further solidified after World War I and then again by the Wall Street Crash in 1929 (as the U.S. became the lender of choice for struggling economies).

By the end of World War II, the USA held the majority of the world’s gold, and most economies had abandoned the gold standard. The result was that the dollar officially became the world’s reserve currency as per the Bretton Woods Agreement in 1944 and has since facilitated the majority of global transactions.

Despite the shaky performance of the dollar and the U.S. economy in recent years, the central bank system continues to perpetuate the dollar’s dominance. Central banks hold large amounts of dollars to facilitate international trade while stabilizing economies with various financial instruments.

The widespread use of the dollar as a measure of trade in global transactions creates a worldwide demand for the currency. Thus, it continues enhancing its worldwide value while reinstating its status as a safe haven.

Some of the dollar’s strength stems from enduring perceptions around the stability of the U.S. economy. Investors worldwide have a level of confidence in the U.S. dollar amidst high inflation rates, unstable economies, and stunted economic growth exhibited in other economies. Hence, worldwide investors view the U.S. dollar as a safe haven with a proven track record in the market with high stability and liquidity.

Quite recently, the COVID-19 pandemic brought about market distress and failures. Despite a shaky domestic performance, the U.S. dollar remained a safe haven currency that flexed its stability in the world economy with deep and liquid financial markets. And regardless of rising geopolitical tensions brought about by war and conflict across the globe, investors continued stocking up on the U.S. dollar.

Role of central banks in monetary policies

Central banks maintain a fundamental role in managing monetary policy decisions of the U.S. Federal Reserve.

The Fed manages interest rates that influence borrowing costs, open market operations, investor sentiments, and inflation expectations. The high-interest rate of the U.S. dollar in correlation to other countries’ currencies leads to an influx of foreign capital, thus leading to high demand for the dollar while stabilizing its strength.

Moreover, actions from the U.S. Federal Reserve and other central banks influence the major flow of liquidity that centers around the theory’s core.

An example of a central bank monetary policy is quantitative easing (Q.E.) during a market failure, where central banks inject more money into the economy to ease the pressure. This leads to an increase in the supply of dollars in the global financial system.

Central banks thus help ensure dollar dominance by determining the amount of money in circulation at any given time, with the aim of facilitating the economic objectives of the hour.

Impact on the global economy

The continued dominance of the U.S. dollar has far-reaching implications for the global economy. Different sectors of global economies remain highly dependent on the performance of the U.S. dollar. Here is a look at a few of these sectors:

International trade

International trade at the global scale remains highly dependent on the performance of the U.S. dollar on the market scale. The stronger the dollar, the cheaper the imports into the U.S. This causes a knock-on effect that lessens the price burden on consumers. Conversely, this limits the competitiveness of the country’s exports.

Moreover, other countries, especially developing countries with weaker currencies, will pay high rates for imports. The result is trade imbalances in favor of the U.S.

Capital flows and markets

Investors look for substantial returns on their capital. Therefore, it is common for investors to align with the U.S. dollar, which guarantees higher returns. Afterward, this creates increased investment inflows.

These investments result in capital flows that increase asset prices and impact global financial stability. Unfortunately, this means that countries with weaker currencies hold the burden of high-interest rates for servicing public debt.

Effect on other central banks

U.S. dollar strength can influence the monetary policy decisions of other central banks looking to cope with rampant price increases and other economic challenges. These central banks adjust their monetary policies to maintain financial stability while managing exchange rates. Some policy interventions include buying and selling currencies to keep up with the U.S. dollar’s relative value.

Most countries hold the U.S. dollar in reserve, especially for international trade and imports. So, any fluctuations in the U.S. dollar’s value will significantly impact the value of these reserves.

Examples in real life

Many examples rooted in crises support the milkshake dollar theory’s claims; that the U.S. dollar will remain key to global economies at the expense of those economies. For example, during the financial crisis 2008, many investors sought refuge in the U.S., thus leading to capital flows.

The resultant capital influx leads to the strengthening of the dollar, which inherently leads to tougher market conditions on other currencies on the global scale. Therefore, countries outside the U.S. feel the impact to a greater extent, even if that impact is felt considerably in the U.S., too.

This is the case, too, when we consider the depreciation of other main currencies on a global scale. The strengthening of the dollar places immense pressure on other currencies, which then leads to devaluation.

The devaluation of a country’s currency significantly impacts its economy, especially when dealing with high levels of debt acquired through foreign currencies. Failure to serve these dollar-denominated debts can cause economic instability.

Is the US dollar under threat?

The U.S. dollar remains a force to reckon with in the financial and global markets. It has been a (relatively) safe haven currency for most investors, financial institutions, and governments. However, recent geopolitical tensions have evoked fears of ‘de-dollarization.’

As a concept, ‘de-dollarization’ is a death killer to the dollar milkshake theory and will end the global dominance of the U.S. dollar after over 100 years at the helm of global economies.

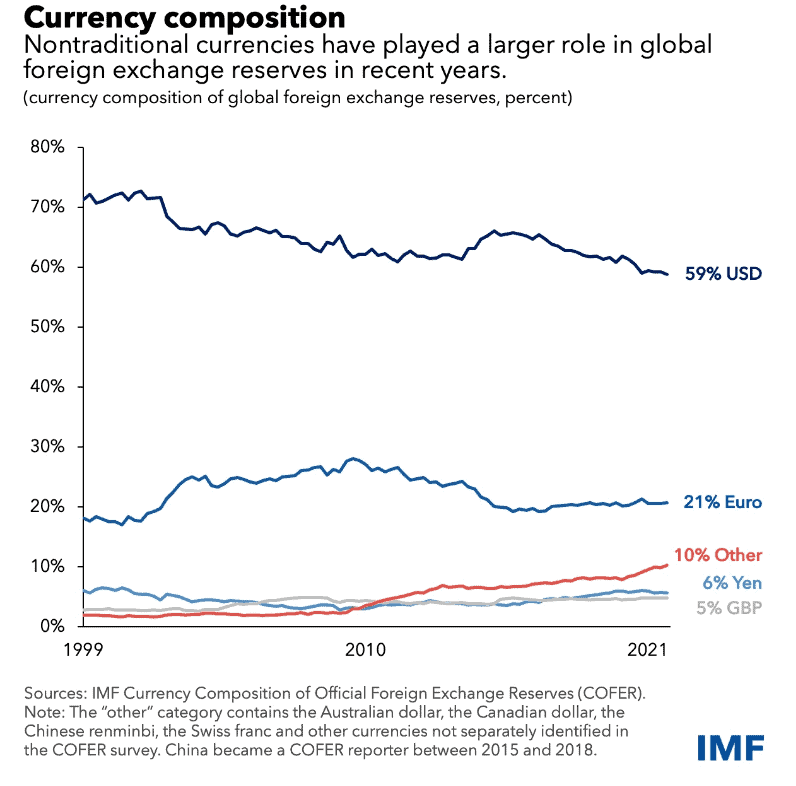

It is true that the dollar’s share of reserve currencies continues to decline, with foreign banks diversifying with the current economic times. IMF data shows that while the U.S. dollar remains dominant in global forex reserves, its share in central banks’ foreign exchange reserves has dropped from more than 70% in 1999.

Global currency composition: IMF

We are witnessing the rise of other currencies that hurt the demand for the U.S. dollar. Moreover, increasing numbers of trade agreements between countries have started dealing with local currencies. This could potentially devalue the U.S. dollar in the foreign exchange markets, thus limiting the dollar’s dominance on the global stage.

A number of countries, from China to Brazil, are increasingly calling for trade to be conducted in currencies other than the U.S. dollar. And, with the economic might of giant players like China ever-growing, the dollar’s status at the top of the global pile is not clear-cut.

The future of the US dollar

The dollar milkshake theory offers one of many perspectives on the current global financial system. While the theory is perhaps an oversimplification of complex global economies, it represents some form of reality; that, despite market turmoil and a clear decline, the dollar remains a powerful currency able to negatively impact the progress of other economies at the expense of its own growth.

Yet, while it may be on the decline, replacing the U.S. dollar as a reserve currency would likely take decades and be a very slow, gradual process. As of 2023, more than 100 years after it first asserted dominance, the dollar remains king.