Have you ever wondered about buying a car, how to do it, and what the whole process would cost? If yes, you are not alone, as many Americans ponder such questions. This article will highlight a popular choice to fund your auto purchase – a loan.

We will explain why it’s the best option, the difference between short and long-term loans, and which to choose. So, if you are ready to find out, let’s look into it!

Car Loans: Process and Available Options

Now that you know the most popular and best option is a car loan, we ought to cover how they work:

- First, apply for a loan from a financial institution (bank or private lender);

- Then aim to qualify and get the money;

- Finally, repay them in installments over a set time.

While this may seem easy, the entire process is much more detailed. Every prospective lender checks your credit score with the 3 credit bureaus and only then decides whether to lend cash. That’s because these agencies collect and maintain credit-related data.

The same is used by lenders and can show the creditworthiness of an individual. You can also check your data with them periodically. They also review your income, age, any equity to your name, etc.

Additionally, you have to choose what type of loan to pick, as they can be short and long-term. These two varieties’ most significant difference is the period over which you have to pay them back.

That is not all; each may have other major/minor advantages and disadvantages based on your contract. That’s why it’s essential to understand loans and their differences to make an informed decision.

Short-term Car Loans

These are typically repaid over a shorter period that spans anywhere from two to five years or less. Their most standard features are:

- Their higher installments;

- Lower interest rates.

A great thing about these two is that you can pay such debt fast. You can avoid most costs that accumulate over time – which usually come with high APR. So, you get a specific sum, buy your car, and within a few years, repay everything. Perfect for those with high incomes or more money to spare.

Long-Term Car Loans

Contrary to the previous ones, long-term car loans last anywhere from five to seven years or more. But that depends on your terms and the lender’s policies. What’s standing out for this type is the lower monthly repayments but an average higher interest rate.

Note that long-term loans, no matter their purpose, are perfect for individuals who want to lower their monthly expenses. These are people who have tight budgets, plan other expenditures, etc.

They must make sure to remember that while the installments are low. The average APR is relatively high; in the long-term, the money they will pay for the car can span from 10-20-30 percent more.

Long or Short: Which One To Pick?

As we have already pointed out, these two types have good and bad sides. It’s up to every individual and their situation which option is better. Additionally, knowing your budgeting game and how to plan your expenses is essential. That’s a primary thing we advise you to consider because you can set your financial goals this way and make your life easier.

A short-term loan will be perfect if you have an ample, stable flow of money each month. You’ll pay off the car and forget these high APR costs and interests. On the other hand, if your budget is tight and you have a lot of expenses, the only option will be the long term.

Putting these aside, another crucial concern when deciding which one is how long you plan to keep the vehicle. A short-term loan may be more suitable if you only want it for a few years. If you think the opposite, long-term will suit you more.

Financing Your Car Purchase

Many decisions must be considered when it comes time to make a significant purchase like an auto. One of these is how you can finance such a purchase. Everybody knows that cars are not a cheap expense, moreover a good, new one.

Given that, you must secure about $30k, maybe $50k beforehand. Now you wonder, what if I don’t have that much? Well, a simple answer exists – borrow them. In fact, that’s normal and is something most Americans do when buying their automobile.

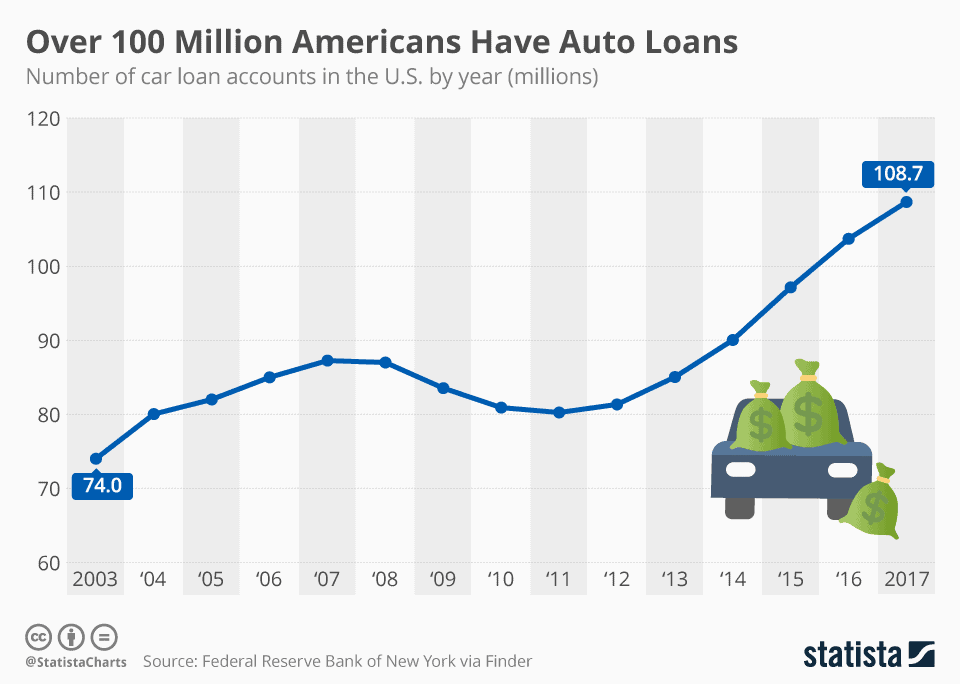

Valid proof that a car loan is your best option is the never-ending, increasing debt that US citizens have over their autos. To be precise, the statistics show a doubling of this debt from 2003 till now. But keep that from bothering you, as an average loan is at most 30 thousand USD or a little over $500 a month.

Can Such Loan Affect My Credit Score?

Yes, it can, both by paying and not paying. We sincerely advise making all payments on time to avoid losing your automobile. Afterward, issues like damaging an existing excellent credit score will follow. With that, all future lenders will be able to see this and issue higher interest.

While your score can be affected negatively, things go both ways. Suppose you pay on time and within the term set by the lender. Your score will increase, your credit history will improve, and you’ll get better conditions on every potential next contract.

Our Final Thoughts

In conclusion, deciding between short or long-term car loans depends on your financial situation. If you pick paying over a more extended period, you’ll rest assured and do your budgeting easier. Contrary, choosing a short-term loan may play you a back joke and make you trade the car to refinance the loan. Ultimately, do your research, find a suitable lender, do your loan-to-finance calculations, and pick the best option for your money.