This post will explain Build a cd ladder. Emergency cost savings are necessary for handling unforeseen expenditures or weathering unpredictable situations like joblessness. Still, practically 30% of Americans don’t have any form of an emergency fund and would need to obtain money to foot the bill if an unexpected expense hits them.

If you do have adequate money to build an emergency fund, it can still hurt to set that money aside. Rate of interest are low these days, and the majority of savings accounts pay practically no interest at all. Even online savings accs tend to pay a rate lower than the rate of inflation, which indicates you’re really losing cash by keeping your cash in savings.

How To Build a CD Ladder Complete Guide

In this article, you can know about Build a cd ladder here are the details below;

A CD ladder helps you remain versatile with your cost savings while eking out a bit more interest. They’re likewise valuable for individuals who tend to let cash burn a hole in their pocket, making it hard to spend all of your savings at once. Also check supply chain management software

What is a CD Ladder?

A Certificate of Deposit, or CD, resembles a special type of savings account. When you open a CD, you pick a term, such as six months, 2 years or 5 years. When you transfer money to open your CD, you make a promise to the bank that you won’t withdraw your cash till the CD’s term ends. If you do require to withdraw money before the term ends, you must pay a charge.

In exchange for your pledge to keep your deposit for a set duration, banks generally use higher interest rates for CDs than they do for savings accounts.

Another function of CDs is that you lock in the interest rate when you open the account. By contrast, banks can alter the rates of interest on savings accounts whenever they ‘d like.

The constraint on when you can withdraw cash from a CD can be a big deal. If your cars and truck breaks down and you require to pay the mechanic bill, paying an early withdrawal fee to get your cash simply makes things more expensive. That is where CD laddering comes in.

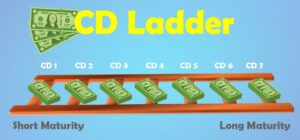

A CD ladder is a sequence of CDs with different maturity dates. As each CD grows, you have the alternative to withdraw your cash or to roll the balance into a new CD. This lets you maintain some flexibility with your cost savings while getting the perks of CDs, such as the higher interest rate.

You can tailor your CD ladder to your needs. If you require routine access to money, set it up so one of your CDs grows every month. If you can wait for longer between opportunities to make a withdrawal, you can have a CD mature quarterly or every six months.

Benefits of CD Laddering

Constructing a CD ladder has numerous advantages.

One is that you capture a higher interest rate than you ‘d make by putting your money into a savings account. Gradually, it will leave you with more money to cover emergency expenses.

To show the benefit of CD laddering, we will utilize Bank ABC (pretend) Saving home builder that has an APY of 1.25%. And after that we would compare that same bank having a CD APY of 1.30%. If you have $11,000 to set aside, you can put it in a savings account and earn 1.25% APY. Over 3 years, you ‘d earn $379 in interest.

If you instead setup a CD ladder utilizing one year CDs, you ‘d make 1.30% APY on your deposit. For 3 years, you ‘d earn $395. You ‘d get practically $100 more just for using a CD ladder. Also check Credit repair companies

Another prospective benefit of CD ladders is that they make it harder to invest all of your cash simultaneously. If you tend to succumb to temptation and spend your savings on desires instead of requirements, a CD ladder locks your savings in the account.

Having to spend a fee to make an earlier withdrawal can help in reducing the temptation to spend your cost savings.

How to Build a CD Ladder

Let’s state you have $6,000 and want to use that cash to build a CD ladder. And you desire the choice to make a withdrawal as soon as every three months.

To do this, you require to divide your $6,000 into 4 sets of $1,500. Then, open one 3 month CD, one six-month CD, one nine-month CD and an one-year CD. Deposit $1,500 into each account.

When your first CD matures, you can easily make a withdrawal. If you desire to keep your CD ladder running, you should roll the balance into a new CD with a 12 month term.

When the very first year elapses, you’ll have 4 CDs with twelve-month terms, with one developing every three months. Every CD makes the rate of interest provided on twelve-month CDs, however you keep additional flexibility.

Depending on your conditions, you can structure your CD ladder nevertheless it makes sense for you. Maybe you only desire access to a few of your cost savings every six months, or you need the possibility to make a withdrawal monthly. Utilizing the correct mix of CDs lets you get the withdrawal frequency that you need.

Best CD Ladder Method for You

The very best CD ladder strategy for you depends upon your goals, resources and requirements. If you have a very large sum of cash available, you can build a long CD ladder to benefit from the interest rates offered by long-term CDs. Typically, long term CDs offer higher APYs than short term CDs.

For example, if you have $21,000 to reserve and want access to cash every three months, you can open eight, $2,500 CDs with terms varying from 3 to twenty-four months. Lots of banks have minimum balance requirements for their CDs, so it can be hard to open so many CDs if you do not have a great deal of money on hand.

If you require frequent access to your savings, the best technique might be to set aside cash in a savings account. Then open a new 1 year CD each month for a year.

Doing this will let you access a few of your savings on a monthly basis and still give you the advantages of a CD ladder. The liability of this strategy is that it takes longer to set up the ladder.

If you highly-value flexibility, you can use non-traditional CDs, such as no-penalty CDs to build your CD ladder. These let you make fee-free withdrawals whenever you ‘d like.

Alternatives to a CD Ladder

If you’re trying to set aside some additional money, there are choices beyond a CD ladder. The simplest and likely most popular choice is to utilize a savings account to hold your emergency situation savings. Online banks generally use fantastic rates for their savings accounts.

Lots of even beat the interest rates offered by CDs at traditional banks. That can make them appealing for keeping an emergency fund. If you desire more versatile access to your savings and possibly greater rates, you could rather open a money market account.

Money market accounts tend to have greater minimum balance requirements and costs than other bank accounts, however combine many aspects of monitoring and savings accounts.

Like checking accounts, most money market accounts offer you the choice to write checks versus your balance. You can likewise get a debit card to make purchases or cash withdrawals from ATMs. However, there are limitations to the number of deals that you can make without incurring a cost.

Like savings accounts, money market acc’s tend to pay interest. Depending upon the bank, this rate could be lower, higher or comparable to the savings account rate.

Typically, the interest rate you get for your money market account increases with the balance of the account. This earns money market accounts ideal for individuals with big amounts to conserve.

If you’re willing to handle extra threat for possibly greater rewards, you could put your savings in a cash market fund, a bond mutual fund or ETF.

These kinds of investments involve danger, and you might lose money if the financial investment performs poorly. Yet, you stand to earn far more than you ‘d get from a savings account, money market account or CD ladder.

Summary

CD laddering is a method that enables you to earn a greater interest rate while keeping the flexibility of using your savings for emergency situation costs.

Selecting the correct structure and establishing your CD ladder can take some time but will pay dividends in the long run. Also check best cloud erp software